This excerpt from The Data Center Almanac focuses on the siting, entitling, and underwriting of data centers.

Overview

The data center development process (think, real estate development) is essentially the siting (where), entitling (how/when), and underwriting (why/who) process that drives a data center concept to construction. It requires thorough due-diligence, involvement from committed stakeholders and the AHJ, and a strong investment thesis with secured funding.

Site Selection

When evaluating where to build a data center many critical factors must be considered with some aspects more nuanced than others. Obviously, environmental and geographical hazards like flood plains, fault lines, or areas with a history of severe weather/environmental impacts should be avoided. The 002-2024 Data Center Design and Implementation Best Practices from ANSI/BICSI outlines a comprehensive list of factors to account for when evaluating locations however, the three most important factors are:

Power Availability

Fiber Availability

Proximity to End User and Workload of Data Center

Find the ANSI/BICSI 002-2024 Standard here for purchase or, if you search creatively, you may find a free PDF somewhere online…it’s a stellar resource on data center 101.

Power Availability

Different types of DC co.’s will have varying minimum requirements of capacity they are seeking from a grid interconnection or another power source (IPP, behind-the-meter, etc.) e.g., Meta and other hyperscalers are evaluating sites of 500MW at minimum but often focusing on locations where they can reach multiple GW, versus smaller colocation or edge groups that may only need 100-200MW or much less (in the case of edge facilities). Of note is that most > 1GW sites are built in phases due to both construction pace but more importantly the ramp-up schedule provided by the power provider, i.e. a utility will tell Meta that it can provide 200MW a year of capacity over the course of five years, totaling 1GW.

DC co.’s will employ internal teams that evaluate locations for future development (as part of larger portfolio planning) but they will also rely on third-party brokers to bring sites to the table for consideration. In this instance, a broker may scout sites, performing initial land and power due-diligence to gauge feasibility and if a location is promising, they will likely option the parcel and begin to shop it out to the larger marketplace of DC co.’s who will then perform their own due-diligence and negotiate terms with the broker.

How do you find power? That is the question everyone wants an answer to. Historically, DC co.’s have worked with utilities to evaluate existing capacity that could power their data centers, requesting utility studies be performed to validate a potential interconnection. They also work with the utilities to assess future (or, planned) power generation development that could serve their data center needs in due time. In today’s times, the interconnection queue is overwhelmed across every ISO/RTO with demand at an all-time high, forcing DC co.’s to get creative in sourcing power. Multiple groups have sought behind-the-meter connections with IPP’s or otherwise formed arrangements, like joint ventures, with power generation companies to colocate new power gen development and data centers in a microgrid or energy park. Many DC co.’s have taken this approach with notable examples including:

Microsoft and Constellation Energy sign a 20 year PPA in partnership to revive the TM-1 (nuclear) reactor at Three Mile Island

Meta and Constellation Energy sign a 20 year PPA for power provided from the Clinton Clean Energy Center

Google’s partnership with Intersect Power and TPG Rise Climate to develop clean energy parks nationwide

AWS partnerships with GE Vernova and Energy Northwest to support development of power generation infrastructure

Stargate group developing on-site nat gas generation in Abilene

Fiber Availability

We’ll come back to permits, power-related and otherwise, at the end but let’s move to fiber. Every data center requires a sufficient and secure fiber connection to connect it to the outside world. This will also play into the next section where we discuss proximity to end user and workload but for now let’s talk fiber at a high-level.

As they evaluate the land and power aspects of a potential site, DC co.’s also want to understand the types, capacity, and latency of fiber available for their future data center. They will assess public and private data and work with carriers to determine if existing fiber in the area will meet their requirements through studies and assessments. As we will discuss shortly, the workload of the data center i.e. what is the purpose of the compute (training LLMs, acting as inference, storing data and records, etc.) will mandate the fiber requirements as certain compute workloads require greater bandwidth and redundancy or otherwise may require closer proximity to the end user (edge).

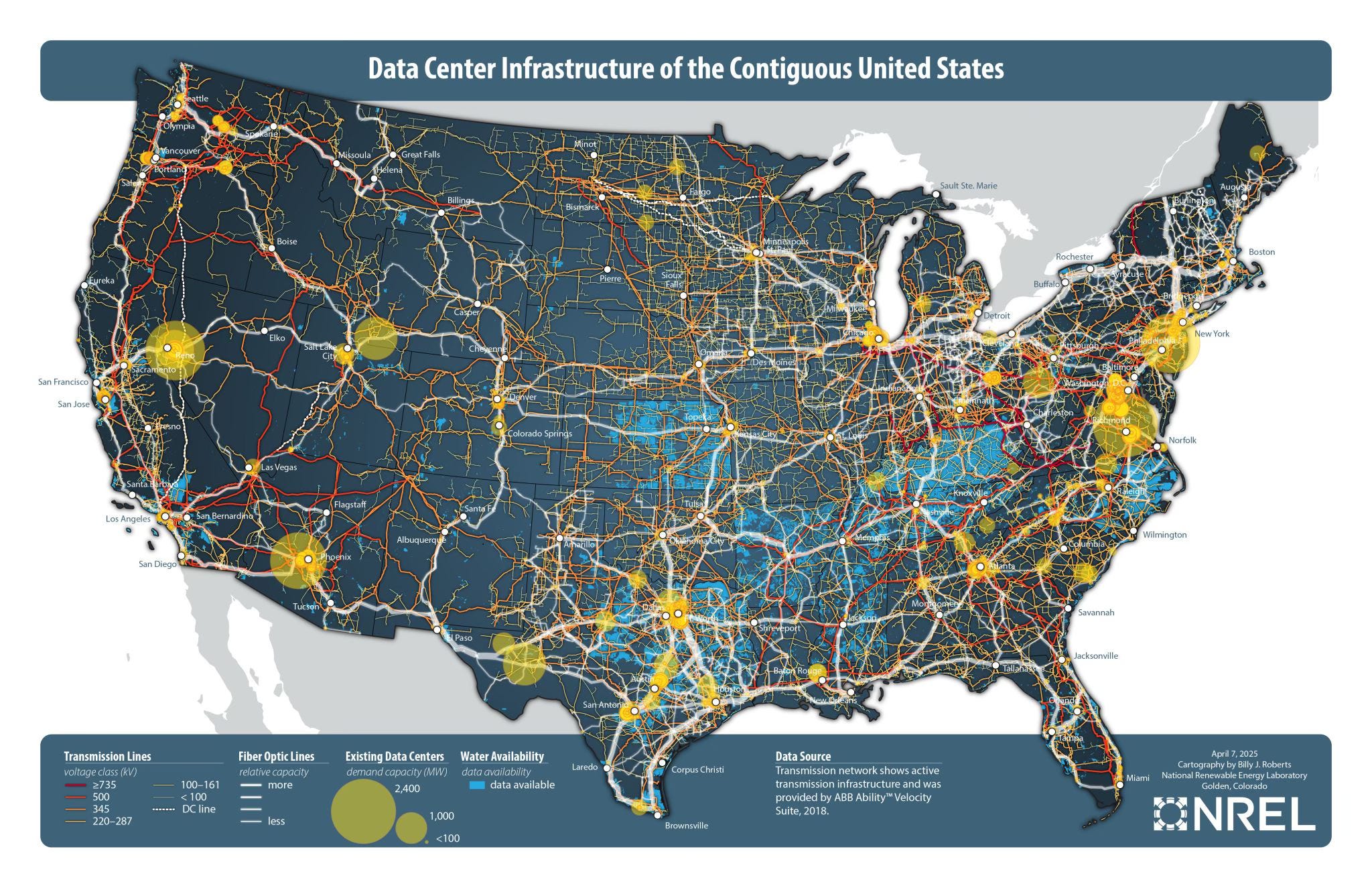

There are different classifications for fiber network hubs with Tier 1 being the most robust (think, centralized with global capabilities), Tier 2 (think, regional interconnections), and Tier 3 (think, local or metro nodes). These hubs and their pathways of interconnections, visualized by the map above, form a sort of network web across the United States.

For example, you may have heard Northern Virginia referred to as “Data Center Alley” and that over 70% of the world’s internet traffic passes through this area daily, but why is that? To make a long story short, in the early 1990s Ashburn became home to MAE-East, one of the original Internet Exchange Points and a primary hub for commercial internet traffic in the U.S. . What followed was dozens of Tier 1 and 2 carriers, like AT&T, deploying fiber infrastructure through this region to access MAE-East. A combination of ample land suitable for building data centers, friendly tax incentives, and proximity to D.C. prompted a flood of data centers to develop in the area. Northern Virginia is regarded as the largest concentration of data centers in the world while other Tier 1 hubs across the country include New York/New Jersey, Chicago, Dallas, Atlanta and a handful of other major cities.

This priority for Tier 1 hubs in major areas contrast other types of data centers, like Bitcoin mining sites, which do not require proximity to a major metro area or as much bandwidth either. This is in part why you see Bitcoin mines built and operated in remote areas, connecting to end users and mining pools via connectivity from Starlink satellites, point-to-point towers, and low tier fiber in certain cases. Large data centers, whether hyperscale/cloud, colocation or edge, usually require multiple fiber pathways for redundancy, a factor not often seen with Bitcoin mines due to cost and availability.

Proximity to End User and Data Center Workload

As a bridge from the previous topic, latency and purpose of a compute workload are two other factors critical to data center site selection. Generally, data centers utilizing large amounts of compute for LLM training do not typically require minimal latency or proximity to a metro area. This means that developers have more freedom in the locations they can evaluate. This is in contrast to other types of data centers, like edge facilities, which are smaller installations and must be located in close proximity to the end user and maintain low latency. For example, companies looking to utilize their now-trained LLMs for inference will look to edge facilities close to metro areas or enterprise users for both commercial purposes and because inference requires lower latency than training. Another example is a critical enterprise or commercial user, like a government agency, large bank, or hospital, that requires low latency and thus, the data center must be nearby to facilitate faster operations required by these types of end users. Edge data centers are typically much smaller in terms of foot print (square feet) and power capacity (megawatts), which also aids in (ideally) faster and easier entitlement and construction timelines.

The past decade has seen an explosion of large hyperscale and cloud data centers as companies seek enough power to train their large LLM clusters however, the development of edge facilities will continue to rise as AI companies move from training LLMs towards inference deployments and continue to strike deals with enterprise and commercial users.

Informative sources on this comparison between training and inference infrastructure requirements are covered in Johan Arts’ post, and Aivres blog post.

Entitlement

This section will include information on items like studies and assessments that could be categorized under “Site Selection”, along with more entitlement-focused items like zoning and land use permits.

As with large commercial/industrial developments, “entitlement” refers to the legal and regulatory approvals required to develop a project on a specific parcel of land. These approvals, rights, or permissions are granted by a governing authority and legally allow a landowner or developer to proceed with the construction of a data center.

The governing authority or AHJ (authority having jurisdiction) is typically a combination of local, state and federal actors that require different levels of scrutiny when evaluating a data center proposal. A planned data center will require approvals like:

Zoning Approval: confirms that the site’s zoning allows for data center or industrial use

Special Use Permit: if the data center isn’t by-right, a special use or conditional use permit is needed

Site Plan Approval: municipality approval of the layout, access roads, utilities, and stormwater

Subdivision/Plat Approval: if the land parcel needs to be divided or reconfigured

Environmental Permits: includes air quality, noise, water discharge, etc.

Building Permits: approval to begin construction based on approved plans

Utility Agreements: commitment from power, water, and telecom providers to serve the site

Traffic/Access Approval: DOT or local AHJ approval for access roads and traffic impact mitigation

Important to note is that entitlements are rights to develop under law or ordinance, whereas permits are specific implementation approvals. What this means is that just because a site has now been sufficiently entitled, permits must be applied for and approved to begin activities like site grading or construction.

As you may have seen, proposed data center developments often run into pushback from an environmental basis and local neighbors. Like with other real estate developments, public hearings are usually required and we have seen communities reject data center developments due to concerns over noise, pollution, or other objections. Data center developers also face significant hurdles with environmental approvals, most notably concerning air quality (if they are running backup generators, for example) and water usage/discharge (how much water will they require from the local infrastructure/what are plans for water remediation). Steps have been taken on both the design front, like closed loop cooling systems that require little-to-no water from the AHJ or backup batteries that are more environmentally friendly than diesel generators, and the AHJ and policy side, with certain municipalities offering expedited entitlement/permit reviews and other groups providing policy recommendations to help inform regulators.

A recent example of this policy push is Anthropic’s latest paper, Build AI in America, wherein the AI company outlines a number of recommendations to expedite both data center and power generation developments. I highly recommend reading the paper in full here. The Anthropic team does a great job succinctly covering the major issues facing grid expansion and data center development, with intelligent recommendations on ways to overcome these challenges. Ultimately, it will be up to regulators across all levels of government to evaluate and take action.

Studies and Permits

As mentioned, there are a number of studies conducted as part of the initial due-diligence phase, as well as a number of permits required once a site has been entitled. I will be releasing a complete piece on studies and permits as part of this ongoing Data Center Almanac series however, here’s an overview:

Common Due-Diligence Studies

Phase I/II ESA (Environmental Site Assessment)

Wetland and Protected Habitat Study

Cultural and Archaeological Study

Threatened and Endangered Species Study

Geotechnical Report

Topographic Study

Electrical Load Study

Water and Sewer Study

Telecom and Fiber Study

Traffic Impact Study

Generator Emissions and Air Modeling

Acoustic Study

Zoning Compliance and Usage Confirmation Letter

Title Commitment and ALTA Study

Common Permits and Approvals

Grading Permit

Erosion and Sediment Control (ESC)

Stormwater Pollution Prevention Plan (SWPP)

Building Permit(s)

Foundation Permit

MEP Permits

Fire Protection and Life Safety Permit

Air Quality Permit

Utility Connection Approval

Encroachment and/or Right-of-Way Permit

Just as every data center design and every AHJ will differ, so will the extent of required permits. Some areas may require less permitting to begin construction whereas other areas will not allow any land work (site clearing or grading) until certain approvals have been granted. It is important to understand the requirements of the AHJ in your desired data center locale, as well as state and federal requirements that must be met in order to proceed. Each of these entitlements, permits, and approvals will have expected timelines and costs associated that must be factored into the larger project schedule and budget.

Permits will be covered in greater detail within the “Preconstruction” chapter of The Data Center Almanac series.

Underwriting

Not unlike any other development, a data center cannot be built without sufficient and secured funding. There are a number of smaller costs associated with site entitlement and permitting, but for the larger CapEx budget a financial structure must be determined as part of overall project planning. This section is full of nuance as every deal will vary in capital structure and terms. For example, a large hyperscaler like Google is well capitalized and may not require as much third-party funding, versus a smaller DC co. or other investment group (like a family office, lender, REIT, or development group) that may be able to cover a portion of the build-out bill but not the entirety of it.

The underwriting of any real estate development, including data centers, essentially evaluates the risk, feasibility, and ROI of the investment (here, building a new data center). The underwriting team will evaluate existing information (site due-diligence) as well as help determine what additional information is needed to analyze the feasibility of the development as they begin to model out the CapEx and OpEx in an initial pro forma.

One important item that covers this entire process (selection/entitlement/underwriting) is that of incentives. Certain AHJ’s will offer a variety of incentives that influence data center development and carry financial and operational implications that are factored into the overall underwriting process as well as the initial site selection. These incentives vary but commonly are tax-related, entitlement/permit-related, or workforce development-related. From a CapEx perspective, many AHJ’s offer sales tax breaks or abatements, grants or other industrial revenue bonds to attractive data centers to their communities.

Capital Structure

Again, every deal will differ greatly in terms of capital structure due to the players involved. In general terms though, you could think of capital structure of a data center deal as follows:

Senior Debt: infrastructure lenders, REIT debt, private credit funds

Preferred Equity / Mezzanine Debt: real estate private equity, structured credit arms

Common Equity: developer capital, sovereign wealth funds, infrastructure funds

In very general terms, you could think of senior debt representing 50-70% of the cap stack, preferred equity/mezzanine debt as 0-20%, and common equity as 20-40%.

Senior debt is typically bank loans, construction loans, or project finance debt from lenders or REITs. Pref. equity and mezzanine debt is higher-yield subordinated capital between equity and senior debt. Lastly, common equity comes from the developer or other limited partners.

Colliers Data Center Marketplace Report 2025 highlights a number of financial players that have provided capital towards data center developments, see page 7.

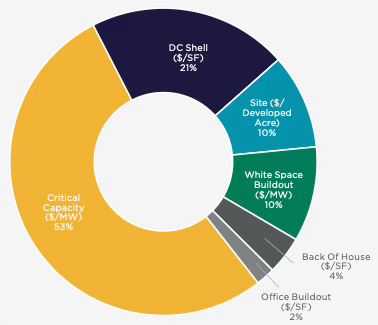

As part of the pro forma, the project budget will be evaluated in common buckets like:

Land and Site Work (5-10%)

Hard Costs i.e, Construction (45-55%)

Soft Costs i.e., Design/Legal/Insurance (10-15%)

Developer Fee and Contingency (5-10%)

Fit-Out or Tenant Improvement (15-25%)

As we will dive into further in the Preconstruction section of The Data Center Almanac series, MEP equipment and servers/GPUs make up the majority of costs. A nice report to reference is Data Center Development Cost Guide 2025 from Cushman & Wakefield.

Another primary factor impacting the underwriting of a data center deal is the confirmation (or lack thereof) of an incoming tenant. For example, certain considerations can be made if a large anchor tenant like Google is confirmed for the planned capacity, but sometimes projects are built in a more speculative fashion where not all of the planned capacity has been spoken for yet. This is similar to spec industrial builds, where a company may build a large industrial complex with a varying amount of the future space already under lease agreements.

If a large hyperscaler is developing a new site for their use exclusively, the capital structure will obviously look much different. These large tech giants like AWS, Google, Meta, Microsoft and Oracle typically have the capital to self-fund these developments with corporate equity, internal cash, and possibly, corporate debt.

The tenant/lease aspect is an important factor impacting the pro forma but other risk factors must be modeled too. These risks could include impacts from tariffs, regulatory delays, geographic/industry demand, and construction risk.

Naturally, every data center development deal will differ in complexity, scale, and structure and as such, the pro forma will attempt to best forecast the risks/returns of the overall project and capital structure supporting it.

To take things a step further, the Total Cost of Ownership (TCO) of the data center, a combination of initial CapEx and the long-term OpEx of the facility across a 20-30 year lifecycle, will be considered during the underwriting. A general rule of thumb is CapEx is around 70% and OpEx is around 30% of the TCO. We will dive into OpEx in greater detail in a future Data Center Operations chapter. To note as well is that unlike traditional commercial/industrial builds, data center CapEx and OpEx is viewed through the metric of cost per megawatt ($/MW), in contrast to cost per square foot ($/SFT). This is due to the nature of data centers being power intensive facilities, with the key factor driving both CapEx and revenue being power, not square footage. This is also reflected in power purchase agreements (PPA) based in terms of $/mw, as well as tenant pricing in $/KW/month, for a colocation facility.

A few helpful articles I found are Financing for New Data Center Construction: An In-Depth Guide, by Patrick Lam, and, Why there is no silver bullet for data center financing, by authors at EY. I am impressed with a number of creative financing strategies we have seen recently and continue to watch out for non-traditional players entering the space, from federal and state infra. funds and international investors, to commercial groups and companies historically not involved in data centers.

Summary

In sum, data center site selection is competitive, data center entitlement is time consuming and challenging, and data center underwriting is complex and creative. Much greater detail could be spent on each of these subjects but hopefully this post provides a decent overview for the lay person looking to learn more.

I would highlight the value of reading Anthropic’s recent report, linked earlier in this post, as well as the Resource Adequacy Report from the U.S. Department of Energy, published a few weeks ago. The DOE report is a proper deep-dive into the current state of the U.S. power grid, specifically as it relates to data center demand, and is a topic we will cover more in a future post.

Drop me a comment with your thoughts on this post- What are the biggest challenges you’ve seen with site selection and entitlement? What underwriting strategies have impressed you with large DC projects? Any good reports or information you’ve found that helps supplement the topics in this post? I always appreciate the input from readers and other industry professionals.